Ghana's Fintech Regulation: Is a 'Hybrid Approach' the Answer?

Between Traditional Financial Regulation and Innovation Promotion, African Financial Authorities Face a Critical Choice

- •A Ghanaian financial expert has called for 'hybrid regulation' combining traditional approaches with innovation promotion in fintech regulation.

- •Existing regulations were designed around banks and cannot keep pace with fintech innovation, leaving financial authorities facing a dilemma between stability and fostering innovation.

- •The proposed approach applies the same regulations to the same services while adjusting intensity based on scale, and manages innovation through regulatory sandboxes.

Fintech Reshaping Africa's Financial Landscape

Ghana and other African nations stand at a crossroads in fintech regulation. As fintech innovation fundamentally transforms how financial services are delivered, the limitations of traditional regulatory frameworks have become increasingly apparent.

According to an analysis contributed by Dr. Richmond Akwasi Atuahene to Ghana's The Business & Financial Times, fintech is characterized by the disintermediation and decentralization of financial services. Rapid technological change, dramatic shifts in business models, and cross-border, cross-sector expansion are all happening simultaneously.

Fundamental Limitations of Traditional Regulatory Frameworks

Existing financial regulations were designed on clear premises. Financial service providers meet certain standards to obtain licenses, and regulatory authorities control excessive risks. Banks and financial institutions monopolized intermediary roles while authorities supervised them.

But fintech has severed this chain. The Financial Stability Board (FSB) defines fintech as "technology-enabled innovation in financial services that could result in new business models, applications, processes, or products." The problem is that such innovation occurs outside traditional financial institutions, outside existing regulatory frameworks.

Dr. Atuahene notes that "for many years in many countries, fintech was unregulated" because "while regulatory authorities focused on traditional banks, existing regulations didn't fit emerging fintech companies."

The Dilemma: Stability or Innovation?

Financial authorities face dual pressure. On one hand, they must adapt regulations to innovations already in the market, while on the other, they must promote innovation to prevent their markets from falling behind.

Fintech has the potential to increase efficiency, reduce costs, and expand financial access. Particularly in Africa where banking infrastructure is weak, fintech is viewed as a key tool for financial inclusion. However, existing regulatory objectives such as consumer protection, anti-money laundering, and systemic risk management cannot be abandoned.

The 'hybrid regulation' proposed by Dr. Atuahene offers an answer to this dilemma: combining traditional entity-based regulation with activity-based regulation.

Core Principles of Hybrid Regulation

1. Same Service, Same Regulation The same regulations apply to identical financial services regardless of provider. Whether it's a bank or a fintech startup, if they provide payment services, they follow the same standards.

2. Proportional Regulation Regulatory intensity is adjusted according to company size and risk level. Requiring small-scale fintechs focused on micro-transactions to meet the same capital requirements as large banks only stifles innovation.

3. Regulatory Sandbox Allows new services to be tested in controlled environments. It acknowledges the possibility of failure while managing risk to prevent system-wide contagion.

The Future of African Finance [AI Analysis]

If Ghana and other African nations successfully establish hybrid regulatory frameworks, there's potential to achieve both financial inclusion and innovation. As the success of mobile money demonstrates, Africa has experience leapfrogging limitations in traditional financial infrastructure through technology.

However, regulatory capacity is crucial. To understand rapidly changing technologies and business models, and to supervise cross-border services, building expertise and international cooperation are essential. If regulations are too loose, consumer harm and systemic risks increase; if too strict, innovation will migrate to other countries.

Ultimately, fintech regulation is the art of balance. The world is watching to see whether Ghana and African financial authorities can find this balance point through hybrid regulation.

댓글 (4)

간결하면서도 핵심을 잘 정리한 기사네요.

Fintech에 대해 더 알고 싶어졌습니다. 후속 기사 부탁드립니다.

그 부분은 저도 궁금했습니다.

기사 잘 봤습니다. 다른 시각의 분석도 읽어보고 싶네요.

More in Special

The Corsican Mafia Exposed: Breaking a Century of Silence

AI-Generated Fake Person Used to Sell Dubai Flight Seats

Facebook Groups Traded Endangered Species Using Code Language — Indonesian Broker Network Exposed

G6 Alliance Declares Support for Hormuz Strait Security... Reverses Stance Under Trump Pressure

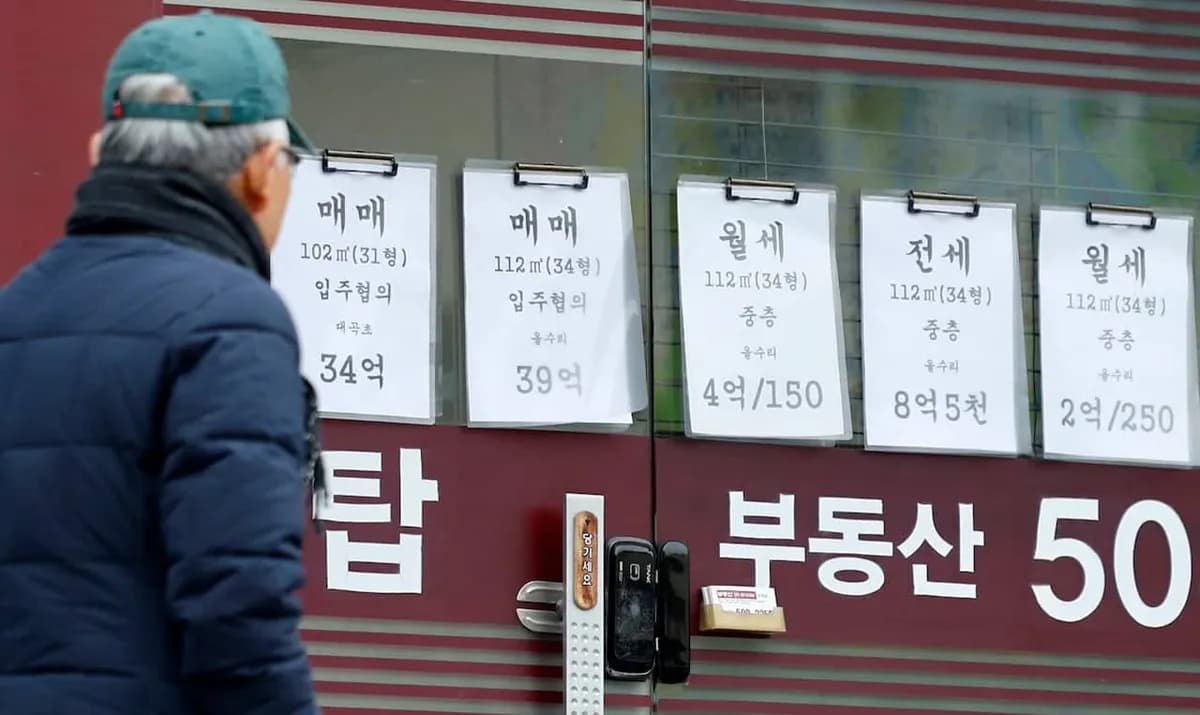

Seoul's Average Monthly Rent Surpasses 1.51 Million Won as Soaring Official Property Prices Trigger 'Housing Cost Bomb'

Rihanna Tops Spotify Without New Album for 10 Years, Proving Power of Catalog

Latest News

이스라엘, 헤즈볼라 무기 통로 레바논 다리 공습

이스라엘군, 헤즈볼라 무기 통로 레바논 다리 공습

중동행 전세기 전쟁보험료 최고 7천500만원

중동행 전세기 전쟁보험료가 최고 5만달러(7천500만원)로 상승

이란 탄도미사일, 이스라엘 방어망 뚫고 160명 부상

이란 탄도미사일이 이스라엘 방공망을 통과해 160명 부상

Middle East Conflict Drives Manufacturing Outlook to 10-Month Low

The Korea Institute for Industrial Economics & Trade survey shows April manufacturing outlook PSI plummeted to 88, falling below baseline for the first time in 10 months.

Lee Jae-myung Administration Excludes Multi-Home Officials from Real Estate Policymaking

President Lee Jae-myung has ordered the exclusion of multi-home owning public officials from all real estate policy processes.

Southeast Asia Growth Forecasts Cut Amid Oil Price Surge, Threatening Korean Exports

Maybank Research has downgraded ASEAN-6's 2026 growth forecast from 4.8% to 4.5%.

Volkswagen CEO Says Germany Should Learn from China's Industrial Strategy

Volkswagen CEO stated that Germany should learn from China's systematic industrial planning approach.

Reddit Considers Face ID to Block Bots While Maintaining Anonymity

Reddit is considering implementing biometric authentication systems such as Face ID and Touch ID to block AI bots while maintaining anonymity.